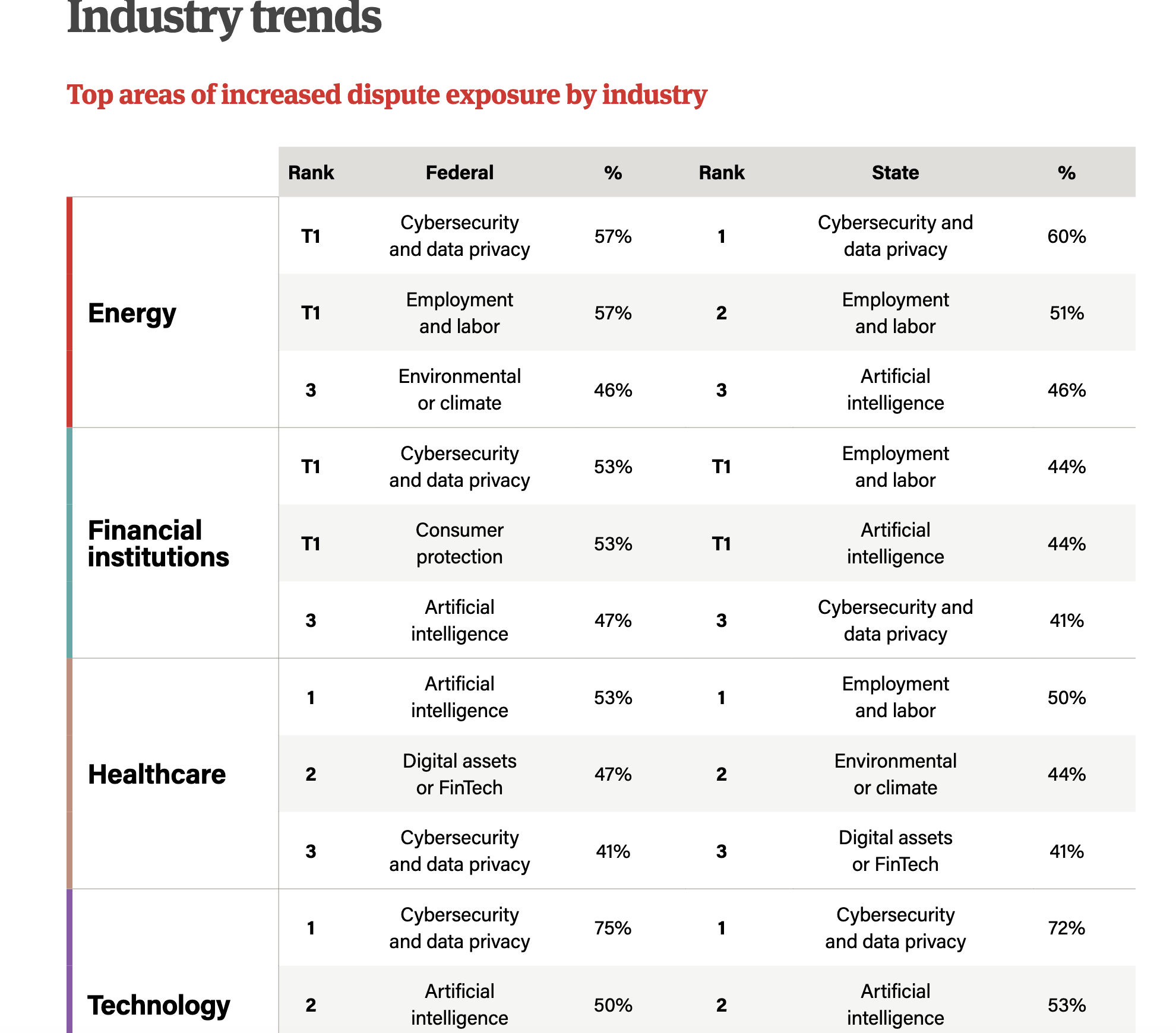

The technology sector is navigating one of the most challenging litigation environments in recent memory. Norton Rose Fulbright’s 2026 Annual Litigation Trends Survey: A Midyear Industry Pulse reveals that 75% of tech respondents have seen increased legal exposure related to cybersecurity and data privacy at the federal level, with 72% reporting similar rises at the state level. These figures position tech as the industry facing the highest escalation in these risks, far outpacing initial expectations from earlier in the year.

Released in June 2026, this midyear pulse surveyed 135 corporate counsel across energy, financial institutions, healthcare, and technology sectors—representing a focused snapshot of the broader 2026 Annual Litigation Trends Survey. The results underscore a rapidly evolving landscape where sophisticated cyberattacks, accelerating AI adoption, fragmented regulations, and aggressive state enforcement are converging to create unprecedented compliance and litigation pressures for tech companies. For privacy professionals, compliance officers, in-house counsel, and business leaders, these insights offer a critical roadmap for understanding and mitigating emerging risks.

Executive Summary: Litigation Risks Accelerating Faster Than Expected

The midyear findings paint a concerning picture. Across the four key industries, more than half of respondents (56% federal, 53% state) reported increased dispute exposure in cybersecurity and data privacy since the start of 2026—significantly higher than the 29% who anticipated such growth in late 2025. AI-related risks are also materializing rapidly, with 46% noting increased federal exposure and 42% at the state level. Data breaches remain the top trigger for class actions (51% overall, 69% in tech), while product launches and AI deployments are emerging as significant catalysts (41% overall).

Despite these headwinds, there are pockets of progress. Many legal teams report improvements in managing internal budgets (55%), outside counsel costs (71%), and data management practices. Technology and energy sectors stand out for stronger gains in litigation readiness. However, the overall message is clear: risks are outpacing preparedness in critical areas, particularly for tech companies operating at the intersection of innovation and regulation.

Tech Sector Spotlight: Highest Cybersecurity and Privacy Exposure

Technology respondents consistently report the most acute increases. The 75% federal and 72% state figures for cybersecurity and data privacy exposure highlight the sector’s unique vulnerabilities. Tech companies serve as both prime targets for attackers and critical infrastructure providers, often bearing secondary liability for customer or third-party impacts. Data breaches top the list of class-action triggers at 69%, reflecting the high-stakes nature of incidents involving personal data at scale.

AI compounds these challenges. 50% of tech respondents reported increased federal AI-related exposure, and 53% at the state level. Specific AI risks cited include privacy/data protection violations (56%), bias/discrimination claims (around 50%), intellectual property disputes, and regulatory investigations. This distributed risk profile—varying by revenue size and use case—makes uniform mitigation strategies difficult. Lower-revenue organizations (<$100M) worry more about privacy, bias, and IP, while larger firms focus on regulatory scrutiny and employment decisions involving AI.

Drivers Behind the Surge in Exposure

Several interconnected factors explain the rapid escalation. First, the sophistication and volume of cyberattacks continue to grow, fueled by AI tools that help adversaries identify vulnerabilities and automate exploits. Geopolitical tensions have heightened focus on critical infrastructure, prompting federal advisories and increased scrutiny. Second, the regulatory patchwork—federal rules evolving alongside aggressive state actions—creates compliance complexity. State attorneys general are stepping in where federal enforcement may have eased, leading to parallel investigations and multijurisdictional defense burdens.

AI adoption accelerates everything. As organizations integrate generative and agentic AI into products, operations, and decision-making, new liabilities emerge around data inputs/outputs, bias in algorithms, and transparency failures. Employment-related AI uses (e.g., hiring tools) add another layer, intersecting with labor laws that vary by state. The survey notes that AI is “shedding new light on existing legal problems and intensifying the associated risks,” with the speed of evolution outpacing organizational adjustments.

Class Action Landscape: Breaches and AI Deployments Dominate Concerns

Class actions remain a primary vehicle for accountability and exposure. Data or cybersecurity breaches lead at 51% overall and 69% in tech. Even “small” incidents can trigger massive statutory damages and multi-state claims, making them uniquely high-stakes. Workforce changes (layoffs, policy shifts) follow at 47%, while product launches or AI-enabled deployments are cited by 41%—with healthcare at 53% but tech also highly concerned due to consumer-facing innovations.

This broadening of triggers signals maturing plaintiff strategies. Litigants are leveraging novel theories around AI harms, from discriminatory outcomes to privacy invasions in training data. For tech companies, this means every new feature rollout carries litigation potential, necessitating rigorous pre-launch assessments.

AI Risks: Fragmented but Pervasive

The survey highlights a “fragmented AI risk landscape.” No single issue dominates, but privacy violations (47%), bias/discrimination (43%), regulatory investigations (42%), and employment decisions (39%) lead. Risks vary by industry and company size. For tech, IP disputes around training data and outputs are prominent, alongside trademark concerns with AI-generated content. Larger organizations face more regulatory heat, while smaller ones grapple with foundational privacy and bias issues.

This distribution reflects AI’s pervasive integration. Whether in customer service chatbots, recommendation engines, or internal analytics, each use case carries distinct liabilities. The overturning of Chevron deference (mentioned in related discussions) may further complicate federal regulatory predictability, pushing more disputes into courts and states.

Litigation Readiness: Signs of Progress Amid Challenges

Not all news is negative. 55% of respondents report improved management of internal legal budgets, and 71% say outside counsel costs have stabilized or eased. Tech respondents are more optimistic about overall readiness improvements, including data management and security practices (53%). Lower-revenue organizations show the strongest gains in several areas, possibly due to nimbler structures. AI governance has improved for both small and large firms (50%).

However, regulatory and compliance complexity remains a persistent headache for the majority. Cross-functional coordination has improved for half of respondents, but sustained investment is needed to keep pace with threats.

Comparative Insights Across Industries

While tech leads in cyber/privacy exposure, other sectors face distinct pressures. Energy grapples with regulatory and environmental intersections; financial institutions with fraud and consumer protection; healthcare with patient data sensitivities and AI in diagnostics. The survey’s industry breakouts (detailed on pages 11-14 of the report) reveal tailored risk profiles, but cyber and AI themes cut across all. This interconnectedness means tech solutions often underpin risks in other verticals, amplifying systemic exposure.

Practical Strategies for Tech Companies to Mitigate Risks

Addressing these trends requires a multi-layered approach. Here’s an expanded set of recommendations:

-

- Robust Vulnerability and Breach Management: Implement continuous monitoring, risk-based patching, and zero-trust architectures. Develop playbooks that address both technical response and regulatory notifications across jurisdictions. Regular tabletop exercises simulating high-impact breaches are essential.

-

- Comprehensive AI Governance Framework: Establish cross-functional AI review boards. Conduct DPIAs for all high-risk uses. Implement bias audits, transparency documentation, and human oversight protocols. Consider “Sealed” or high-privacy modes for sensitive applications.

-

- State and Federal Compliance Alignment: Map obligations under CCPA/CPRA, state breach laws, and federal guidelines. Engage proactively with AG offices and industry consortia. Track legislative developments in key states like California, New York, and Virginia.

-

- Enhanced Third-Party and Supply Chain Oversight: Vet vendors rigorously, enforce strong contractual protections, and monitor for inherited risks. Many breaches originate through partners.

-

- Cost-Effective Legal Operations: Leverage technology (including secure AI tools) for document review and routine tasks. Build stronger internal capabilities to reduce reliance on outside counsel while maintaining quality.

-

- Insurance and Risk Transfer: Review cyber policies for adequate limits, sublimits on regulatory fines, and coverage for AI-specific claims. Negotiate tailored endorsements.

-

- Culture and Training: Foster organization-wide privacy and security awareness. Tie executive compensation to compliance metrics and conduct regular simulations.

-

- Documentation and Defensibility: Maintain detailed records of risk assessments, decisions, and mitigation efforts. This “paper trail” is invaluable in investigations and litigation.

Broader Implications for the Tech Industry and Privacy Compliance

The survey arrives amid a perfect storm: post-Chevron regulatory uncertainty, state-level activism, AI proliferation, and sophisticated adversaries. For Captain Compliance readers, the intersection of privacy, cybersecurity, and AI governance is no longer siloed—it’s central to business survival and growth. Organizations that treat these as strategic imperatives, rather than cost centers, will differentiate themselves.

Consumer trust hangs in the balance. High-profile incidents erode confidence, while proactive transparency can build loyalty. Regulators are watching closely; demonstrable accountability through audits, impact assessments, and rapid response can mitigate enforcement actions.

Looking Forward: Preparedness for the Second Half of 2026 and Beyond

As we move into the latter half of 2026, risks are unlikely to subside. Emerging technologies, election-year dynamics, and global events will continue shaping the landscape. Tech companies should prioritize scenario planning, invest in talent (bridging the skills gap in privacy/AI law), and collaborate across sectors for shared intelligence.

The Norton Rose Fulbright midyear pulse serves as both a warning and a call to action. By learning from the data—acknowledging the surge in exposure while building on readiness gains—organizations can navigate uncertainty more effectively. Privacy and compliance teams are at the forefront of this effort, translating complex risks into actionable strategies that protect individuals, safeguard innovation, and support sustainable business growth.